On major decision days, FX charts often appear unusually calm as the market hovers in tight ranges. Then, almost instantly, it turns into chaos. Central bank meetings from the Fed, ECB, or BoE compress a huge amount of macroeconomic expectation into a few minutes of statements, projections, and press-conference remarks. Once released, the market absorbs this information in a single burst, and price action reacts accordingly.

Investor sentiment was shaped by steady (not accelerating) macro signals and a market that is increasingly priced for policy inertia. In the US, inflation remained contained (Dec CPI ~+2.7% YoY; core ~+2.6% YoY), reinforcing expectations that the Fed is unlikely to change rates at its January meeting. With growth data only producing modest surprises (rather than persistent upside/downside momentum), markets continued to treat the near‑term outlook as “stable but not strong,” which kept risk appetite contained and encouraged selective positioning rather than broad risk‑on exposure.

In finance, the yield curve shows how much it costs the US government to borrow for different lengths of time. Most people hear about it only when it inverts, when short‑term rates rise above long‑term ones, because that pattern has historically appeared before recessions. But the yield curve is doing much more than flashing warnings. It is telling a story about how markets see growth, inflation, and future Fed policy.

Major central banks mostly held a steady course amid broadly easing inflation. US price data remained benign – headline CPI was about 2.7% year-on-year in December, about the same as November – supporting expectations that the Fed may only cut rates later in 2026 rather than move quickly.

Traders often scratch their heads when monthly inflation data arrive. One moment markets leap on the latest Consumer Price Index (CPI), the next analysts remind us that the Fed really watches the Personal Consumption Expenditures (PCE) index. Why do we have these two gauges, and why do markets treat them so differently?

The first full trading week of 2026 unfolded with a steady macro backdrop and limited change in central bank expectations. Policy signals across major economies remained broadly consistent with late-December messaging, reinforcing a sense of continuity rather than transition. Inflation trends continue to ease gradually, while growth indicators point to moderation rather than deterioration, keeping investors positioned cautiously but constructively.

Picture the scene: early afternoon on the first Friday of the month. Suddenly, charts across the board start whipsawing – currency pairs go up and down, indices go up and down, and even gold can’t make up its mind. Welcome to Non-Farm Payrolls (NFP) Friday. Once a month, this US jobs report hits the wires and global markets often pause and brace for impact.

As 2025 drew to a close, markets continued to digest the after-effects of aggressive policy shifts in prior years. Q4 2025 didn’t bring new shocks but instead reinforced themes that had been building throughout the year. The quarter provided a moment of relative stability across asset classes, with monetary policy becoming clearer but fiscal constraints coming into sharper focus. This piece explores how Q4 played out across markets, what 2025 taught investors more broadly, and what 2026 may have in store – through a lens of cautious realism rather than bold forecasting.

After the inflation shock of 2022 and 2023, price pressures have finally started to cool. Inflation has not disappeared, but it has slowed, and that phase is known as disinflation. Prices are still rising, just not at the pace that unsettled households, policymakers, and markets a couple of years ago.

Global policymakers enter 2026 with policy divergence and a broadly stable backdrop. In the US, Fed officials have signalled a pause in rate hikes after a 3.50-3.75% policy rate (no hikes likely ahead and only one cut pencilled in 2026). Economic data have shown cooling inflation and modest growth, and markets now see Fed cuts (perhaps two) outpacing other central banks.

Picture this scenario: a central bank raises interest rates, yet the currency weakens instead of strengthening. It sounds counterintuitive, but seasoned traders know it’s not the rate hike itself that matters – it’s what the market expected to happen next. FX markets are forward-looking by nature, meaning they focus on where rates are headed rather than where they stand today.

Markets traded through a holiday-shortened and liquidity-constrained week, with price action driven more by positioning, macro expectations and year-end flows than by fresh data surprises. Several major exchanges were closed for Christmas, while others operated on shortened hours, amplifying moves in otherwise thin conditions.

As the year winds down and the holiday season approaches, financial markets enter a unique environment. Liquidity thins, spreads shift, volatility becomes unpredictable, and trader behaviour changes as institutional desks slow down for the break.

Markets closed out the penultimate full trading week of 2025 grappling with a defining theme: policy divergence. Despite several potential volatility catalysts, investors largely held existing positioning, with mixed US macro data failing to force a meaningful repricing into year-end.

Every December, markets enter a peculiar phase. Liquidity thins, trading desks quieten, sentiment shifts, and yet, historically, a surprising pattern often emerges.

December is one of the most unique months in the trading calendar. With thinner liquidity, shifts in market behaviour, and year-end flows shaping price action, traders need to stay sharp and structured.

Markets entered the week focused squarely on the Federal Reserve, and the outcome delivered little surprise but meaningful consequences. On Wednesday, the FOMC implemented a widely expected 25bp rate cut, lowering the federal funds target range from 3.75%-4.00% to 3.50%-3.75%, formally ending the 4% policy-rate era.

Investors have spent the past two years in a will-it-or-won’t-it debate, wondering if economic growth could really hold up while inflation cooled off. Central banks have been trying to control inflation without triggering a recession, and as price pressures ease, markets keep asking: is this time different?

With long-delayed data finally released post-shutdown, investors welcomed signs of easing inflation, core PCE rose just +0.3% in September. Early-December sentiment surveys ticked up, but labor market softness lingered. Markets expect the Fed to cut rates by 25bps at the December 9-10 meeting. Optimism remains fragile, but most traders now anticipate a third consecutive cut as the Fed aims to cushion a slowing economy.

Markets ended the final week of November on firmer footing as investors priced in a growing likelihood of a Federal Reserve rate cut at the December 9-10 meeting. Softer US data following the post-shutdown backlog and easing Treasury yields helped shift sentiment toward a more dovish outlook.

Every trader has a few dates they circle on the calendar each month. For many, the first Friday sits right at the top of that list. That is when the US Non-Farm Payrolls (NFP) report is released, and it often dictates the mood of global markets for days afterward. Even if you do not trade US equities or the dollar directly, you still feel the ripple effect. NFP has a way of pulling the wider market into alignment because the labour market is one of the cleanest windows into the real economy. When hiring strengthens, it carries a message. When it weakens, that message becomes even louder.

The US dollar has been the dominant force in global markets for the better part of the last few years. Back in 2022-23, the Fed’s aggressive rate hikes and waves of global risk-off sentiment pushed the dollar higher and higher. The DXY hovered in the low 100s, with every Fed speech and CPI print moving the needle. It was the trade that just kept working.

Last week’s backdrop was shaped by the end of the 43-day US government shutdown and cautious tone from central banks. The funding extension cleared a key uncertainty but created a backlog of economic data, with the October CPI report cancelled.

Inflation is a driver of markets. When new inflation numbers come out each month, traders of currencies, stocks, bonds and commodities all pay attention. A sudden rise or fall in inflation can quickly change expectations for interest rates and move markets.

For two years, the dollar’s climb against the yen has been one of the biggest stories in FX, powered by a yawning interest-rate gap between the US and Japan. That gap made shorting the yen almost a no-brainer. But now, things feel… different. The pair is pressing against multi-decade highs, volatility is ticking up, and Tokyo is sounding more urgent. It’s the kind of moment where traders pause and ask: Is this the top?

The US dollar has been the dominant force in global markets for the better part of the last few years. Back in 2022-23, the Fed’s aggressive rate hikes and waves of global risk-off sentiment pushed the dollar higher and higher. The DXY hovered in the low 100s, with every Fed speech and CPI print moving the needle. It was the trade that just kept working.

The biggest story this week was the end of the US government shutdown. Congress approved a continuing funding resolution late Wednesday, allowing federal agencies to reopen and workers to be paid back wages.

In FX (foreign exchange margin trading), strategically choosing the right order method is crucial for maximizing profits. Traders can improve accuracy and risk management by using different order types such as market, limit, and stop orders depending on the situation.

Energy stocks have been on a remarkable run over the past few years, especially after Covid-19. The S&P 500 Energy sector surged nearly 50% in 2021 and 55% in 2022, vastly outperforming the broader market.

FX (foreign exchange margin trading) is a financial transaction where you buy and sell currencies from around the world to seek profits. However, when trading FX for the first time, you may have many questions such as “How do I place an order?”, “How do I decide the position size?”, or “What is a Pip?”.

Markets grappled with mixed economic signals and missing data last week as an ongoing US government shutdown delayed key reports. Investors saw conflicting readings on the labour market – private payrolls rebounded by +42,000 in October according to ADP, but a separate survey showed layoffs surging to 153,000, the highest monthly total since 2003.

Every trader believes they can control risk, until the market reminds them otherwise. This sobering thought underlies the illusion of control in trading. We set entry points, study charts, and place stop orders as if we command the outcome. In reality, technical tools can only control our decisions, not the market itself!

When engaging in FX (foreign exchange margin trading), “risk management” is something you cannot avoid. Among the most important aspects of this is the “Margin Call,” known in Japanese as “追証 (Oishō).”

Central banks are shifting gears. The Fed, ECB, and BoE have all turned more dovish heading into the end of 2025, and rate cuts are now widely expected. Inflation is cooling slowly but steadily, and bond yields are drifting lower. On paper, this should be a sweet spot for low-duration stocks: financials, energy, and defensives that lean on near-term cash flows rather than long-term growth stories.

In FX trading, the concepts of “loss cut” and “forced loss cut” are unavoidable. While many traders have heard these terms, fewer truly understand how they work and why they are so important.

The final week of October delivered a mix of central bank decisions, earnings results, and macroeconomic data. In the US, the Fed cut interest rates by 25 basis points at its 29-30 October meeting, lowering the target range to 3.75%-4.00%.

Are you ready to step into the markets with the knowledge and the confidence needed to succeed? Introducing EC Academy. The trading education hub for a smarter, simpler, and entirely free way to learn trading online.

Success in trading rarely happens by accident. It usually grows out of doing the right things, over and over again. That’s where having a routine makes all the difference.

FX (Foreign Exchange Margin Trading) is an attractive method of trading that allows you to move large amounts of money with relatively small capital through “leverage.” However, this also means that the potential losses can be significant.

The stage is set: inflation is finally cooling toward central-bank targets (US core PCE was ~2.1% in April), and major central banks are talking cuts. The Fed held rates in June 2025 but still pencilled in two quarter-point cuts this year.

“I’m interested in FX, but I’m scared to use real money right away...”

This is where demo trading apps come in handy — they let beginners learn trading with zero risk.

A demo trade is a practice tool that allows you to experience real market movements using virtual funds. It’s perfect for beginners and an essential step for anyone touching FX for the first time.

In FX trading, “spread” is directly linked to trading costs. However, surprisingly few people accurately understand what a spread really is or whether a variable or fixed type suits them better. This article clearly explains the advantages and disadvantages of both types — referencing account types offered by major brokers — in about 2,000 words. At the end, you’ll also find a quick comparison checklist to help you choose the best option for your trading style.

Overseas Forex offers many attractive features not found in domestic FX, such as high leverage, bonus systems, and zero-cut protection. However, with so many overseas FX brokers available, it can be difficult to decide which one to choose.

The oil price surge during early 2025 has made energy costs a primary factor behind inflation growth. The ongoing high US household inflation expectations have led investors to use oil as their inflation protection strategy. The oil market now leads the way in determining inflation rates and dollar value and market sentiment.

As of 2025, FX accounts available to individual investors are broadly divided into “domestic” and “overseas.” The choice between the two significantly affects leverage limits, tax rates, and fund protection mechanisms — making your initial decision a key factor in future performance. This guide explores both options in depth, offering concrete insights to help you find the ideal trading environment.

US markets opened the week in limbo as the government shutdown entered its third week, freezing major data releases. Fed officials stepped into the void, reinforcing a gradual easing bias. Core inflation remains sticky: US core PCE inflation ran about 2.9% year-on-year in August. With the shutdown delaying US CPI (now shifted to late October) markets clung to Fed signals.

FX (Foreign Exchange Margin Trading) is becoming increasingly popular as an investment option. In addition to being easily accessible via smartphone or computer, its appeal lies in the potential to aim for significant returns even with small amounts of capital.

Leverage in trading can feel like a secret superpower, letting you do more with less. But what exactly is leverage? It simply means borrowing funds from your broker to better your trading position beyond what your own cash could fund. Leverage is powerful because it magnifies both gains and losses, so it’s vital for traders to use it wisely.

When starting FX (foreign exchange margin trading), the first thing to pay attention to is the spread. Although the spread may seem like a small difference, it has a major impact on profit and loss as the number of trades increases. This is especially important for short-term traders such as scalpers and day traders.

After two years of rapid interest rate hikes, central banks are finally shifting gears. In 2025, ECB has already slashed its benchmark rate from nearly 4% down to about 2%. The US Fed is also stepping off the brake, delivering its first 0.25% rate cut from a much higher peak and indicating more to come by the end of the year. Not to forget, even BoE has begun trimming rates.

In FX trading, the ability to “read charts” is one of the essential skills for making profits. By visually understanding price movements, traders can grasp market trends and make more rational trading decisions. This article explains the basics of how to read charts and introduces representative analysis methods and chart patterns that even beginners can easily understand.

Markets entered October balancing two competing forces – a Federal Reserve that sounded increasingly open to further easing, and a sudden revival of trade tensions between the world’s largest economies.

Forex (FX) trading offers a major advantage: it’s open 24 hours a day. However, just because you can trade anytime doesn’t mean every hour is equally profitable. Understanding when the market is most active—and when to avoid trading—can help you make smarter, more efficient trades.

If you ask any seasoned trader, they will say that interest rates are the heartbeat of the forex market. That’s because they influence nearly every aspect of currency trading – from massive global capital flows to the day-to-day central bank decisions. In this piece, we will explore why interest rates are the most powerful force in forex, and how even a small change can have a ripple effect on currencies.

After two long years of rate hikes, the pendulum has finally swung the other way. Both the Fed and ECB have started cutting interest rates, easing financial conditions that had been tightening since 2022. But here’s the twist, markets on both the sides aren’t reacting the same way.

In Q3 markets pivoted sharply on policy divergence. The Fed signalled an imminent easing cycle, while many governments moved toward fiscal restraint. Growth and employment weakened enough in the US to prompt a late-September rate cut, even as fiscal policy pulled back.

FX is an investment method that aims to profit from currency price fluctuations. There are many ways to trade, but success requires acting based on a clear strategy, not just simple buying and selling.

When Liverpool FC signed Swedish striker Alexander Isak, the football world took notice, it was a strategic move that showed how champion teams are built with precision and long term planning. In many ways, the process of creating a successful football squad is very similar to how traders build a winning portfolio in the financial markets.

Markets spent most of last week stuck between two narratives: inflation that remains stubbornly high and a Fed that finally made its first cut since late 2024. August’s PCE numbers came in as expected with core prices up 0.3% on the month, 2.7% YoY. Not exactly encouraging, but not worse than feared either. It was just enough to calm nerves after the cut, though investors were left second-guessing whether this was the start of an easing cycle or simply a cautious adjustment.

I’m interested in FX, but I don’t know how to start…”

This article is designed for beginners like you, breaking down how to start FX in 5 simple steps.

Stock markets often move in waves – one sector cools as another heats up. It’s how markets rotate. Recently, the tech-heavy “Magnificent Seven” names have lost steam while cyclicals like energy and industrials have been rallying. This is why traders are eyeing relative strength charts. These charts show which sectors are outperforming and hint at who might lead next. For example, a recent analysis noted consumer discretionary and communications stocks are firmly in the “leading” quadrant on a relative rotation graph, whereas tech is rolling into “weakening” territory. Healthcare is meanwhile just beginning to climb from lagging to improving, suggesting its turn could be near.

“What is FX trading? Since it’s an investment, does it always come with risks? …”

FX is an investment where you can gain significant returns if things go well, but at the same time, there is a risk of losses. In this article, we will clearly explain the basics of FX, as well as the balance between risks and returns.

“I want to try Forex trading, but it looks complicated...” Have you ever thought that? In this article, we’ll explain FX step by step for beginners who want to start trading. We’ll cover what FX is, its basics, how to get started, and the key points to watch out for.

September’s second week was all about balancing softer data with central bank caution and a few geopolitical flare-ups. In the US, the August CPI print came in at +0.4% MoM, pushing the annual rate to 2.9%, its highest level since January. Core CPI held steady at 3.1%, which was enough to reassure investors that underlying pressures aren’t spiralling.

The Japanese yen is at a crossroads. After years of playing dual roles – safe-haven asset and funding currency for carry trades – it faces a turning point. BoJ is hinting at ending its era of ultra-low rates, so will the yen regain its safe-haven shine or remain the world’s favourite funding currency?

September began with investors weighing softer data, cautious central banks, and persistent geopolitical risks.

In the US, the August jobs report set the tone. Payrolls rose by 165,000, below expectations, while unemployment edged up to 4.3%, the highest since 2023.

Here’s a curious thing about the US dollar: it tends to rise when the world is falling apart… but also when the US economy is roaring. Odd combination, right? If things are bad, you’d expect the dollar to drop. And if everything’s great, maybe people would diversify into other currencies. Yet history keeps showing the opposite. Economists call this the Dollar Smile Theory. And once you walk through the idea, it actually feels pretty intuitive.

For decades, Japan has been the land of cheap money. Interest rates sat near zero, sometimes even below, while other countries offered much higher returns. That gap created what traders call the “carry trade.” The logic is simple: borrow yen at almost no cost, swap it into dollars, and invest in US bonds paying 4-5%. The difference becomes your profit.

Global markets rode a volatile week shaped by shifting monetary policy expectations and geopolitical surprises. In the US, Powell’s Jackson Hole remarks landed on the dovish side, signalling risks have tilted toward labour softness and nudging the door open for a September rate cut. At the same time, the Commerce Department revised Q2 GDP up to 3.3% annualised, a firmer base than first thought. Core PCE eased to 2.9% YoY, keeping the disinflation trend intact even as consumer confidence slipped and hiring cooled. Put together, traders leaned into nearly 90% odds of a cut next month.

Markets spent the week waiting for Jackson Hole, and Powell didn’t disappoint. His message was softer than many feared: the Fed now sees the balance of risks shifting, and he even opened the door to a September cut. That was enough to steady nerves after five straight down sessions for Wall Street. By Friday, the Dow was at record highs, the S&P 500 rose, and only the Nasdaq lagged as tech finally cooled.

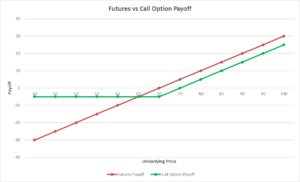

If you’ve ever booked a holiday months ahead just to lock in a flight price, you already understand the idea of derivatives. In markets, they work the same way.

Every trading community, from the smallest retail account to the largest institutional desk, confronts a universal scarcity: finite capital set against infinite market uncertainty.

Picture this. It’s early morning, coffee in hand, and traders everywhere are hovering over their screens. One number is about to drop. It might be the latest inflation figure. It might be the monthly jobs report. Either way, within seconds it’s across news tickers. And, just like that, markets could jump, stumble, or go haywire.

No surprise moves, but no green light for rate cuts yet either

At its July 2930 meeting, the US Federal Reserve kept interest rates unchanged at 4.25%-4.50%. That’s the same level it’s held since earlier this year, and Fed Chair Jerome Powell made it clear they’re not rushing into any rate cuts just yet.

Japan, deflation, and low-rate environments explained.

You’ve probably heard someone throw around the term “liquidity trap” and just moved on. Fair enough, it does sound like one of those textbook ideas economists obsess over. But here’s the thing. It actually matters, and more than you might think.

The financial landscape in Thailand is growing rapidly, with a number of young and experienced traders looking beyond their local options to access gold trading and forex trading markets.

India is home to a growing population of retail traders, from professionals in finance to everyday investors, with more and more people exploring the potential of forex trading and gold trading.

EUR/USD is trading near its highest level of 2025, and on the surface, the trend looks strong. But traders aren’t just watching the price – they’re asking a deeper question: Is this move backed by real demand, or could it be a short-lived spike?